What is CalSavers?

CalSavers is a retirement savings program run by the state of California. It’s designed to help employees save for retirement through automatic payroll deductions, at no cost to the employer.

CalSavers is a Roth IRA (Individual Retirement Account) funded entirely by employees. Employers are not allowed to make contributions. Your only role is to register, set up the employer account, and remit employee contributions for every pay period.

Important Deadline: December 31, 2026

If you employed at least one W-2 household employee in 2024 or 2025, California requires you to register or certify an exemption with CalSavers by December 31, 2026. CalSavers should be sending you information on this requirement via mail in the coming months.

✋Hired your first employee in 2026? You are not subject to this requirement and have no action needed for now.

If you registered in California in 2026, you are not required to register yet. CalSavers will contact you with your specific deadline and instructions when the time comes. No action is required from you right now.

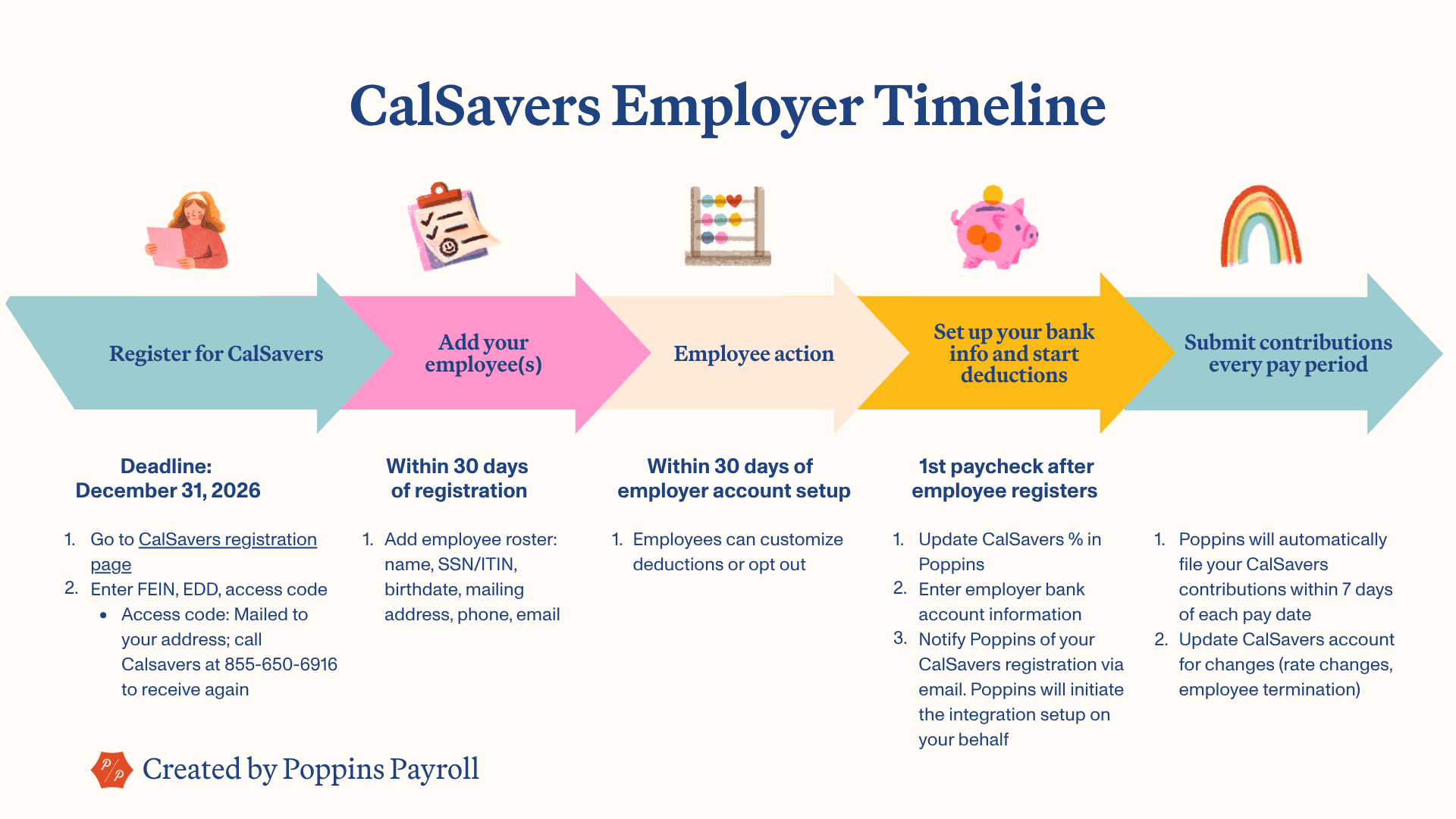

Steps to Complete CalSavers (Full Overview)

Here’s a step-by-step breakdown of what to do, when to do it, and how it all works:

Step 1: Register with CalSavers (by December 31, 2026)

What to do

Visit the CalSavers employer registration page and enter the following information:

- FEIN (Federal Employer Identification Number)

- California payroll tax number (EDD)

- CalSavers access code – this was sent to your mailing address on file with EDD. If you don’t have it, call 855-650-6916 to request it again.

TIP: You’ll find your FEIN and EDD numbers inside your Poppins account under:

Settings → My Account → Account Numbers

Step 2: Add Your Employee(s) (within 30 days of registering)

Once registered:

- Log into your CalSavers account

- Upload your employee roster using their template or enter information manually

- You’ll need this info for each employee:

- Full name

- SSN/ITIN

- Date of birth

- Physical address

- Phone number

- Email address

Poppins makes this easy, just go to: Settings → Employee Info → General Info to view your employee’s details (except SSN/ITIN, which you can find on their W-4 or I-9 form).

Step 3: Employee Action (30 days to enroll or opt out)

After Step 2, CalSavers will email your employee(s) directly.

Within 30 days of step 2, employees must decide on their CalSavers participation. They can:

- Enroll → and start saving automatically

- Opt out → and skip the program entirely

Important: If employees do nothing within the 30 day period, they’ll be automatically enrolled at 5% of their wages deducted each pay period.

Step 4: Set Up Your Bank Info and Start Deductions

Once your employee's 30-day decision window closes (they’ve enrolled or been auto-enrolled):

Add Your Bank Account to CalSavers

CalSavers will email you when it’s time to start making contributions. Before your next payroll:

- Log in to your CalSavers employer portal

- Add your bank account and routing number

- This is the account from which you’ll remit contributions each pay period

Important: The bank information entered in CalSavers should be the same bank information you have provided to Poppins Payroll. This ensures that CalSavers contributions are withdrawn from the same bank account as your household payroll.

Add the Employee’s Contribution to Their Poppins Profile

Poppins will list the exact dollar amount of the deduction on your employee’s paystub — but you’ll need to tell us what percent to deduct:

- Go to Settings → Employee Info → Pay Settings

- Enter the CalSavers Contribution Percentage (typically 5% unless your employee opts for more/less)

- Poppins will now automatically include the contribution in each paystub

Step 5: Notify Poppins of Your CalSavers Registration

Simply email us at info@poppinspayroll.com. This notification allows us to initiate the integration setup on your behalf.

Step 6: Submit Contributions Every Pay Period

Here’s how ongoing submissions work, starting with your first deduction:

First Payroll Deduction

- Your first CalSavers deduction should occur in the first pay period after the employee’s 30-day enrollment window ends

- In Poppins, you’ll still pay employees the net amount (after the CalSavers deduction)

- Separately, log into CalSavers to submit the deducted amount (within 7 days of your employee's pay date)

Each Pay Period After That

- After each payroll run, Poppins will show the deduction amount on the paystub

- You’ll log in to CalSavers to remit contributions within 7 business days of the pay date

- If employees change their contribution rate or opt out, CalSavers will email you directly. You’ll update their payroll settings in Poppins to match

If Employment Ends

- Withhold the final contribution on the last paycheck

- Submit it through CalSavers like usual

- Then, in the portal, mark the employee as “inactive” to end future deductions

CalSavers Resources

- Official CalSavers FAQs: https://www.treasurer.ca.gov/calsavers/

- Employer Overview (PDF): https://www.treasurer.ca.gov/calsavers/CalSavers_Overview_for_Employers.pdf

- Employer Registration Login: https://employer.calsavers.com/

- Access code helpline: 855-650-6916

Have more questions? Let us know, we’re here to help walk you through this. Poppins is all about making payroll and compliance feel doable.

.png)

.png)

.png)