.png)

For most families, it starts small. A few hours of help a week — someone to drive your parent to appointments, handle groceries, keep them company. Manageable. You tell yourself it's temporary.

Then something shifts. A fall, a diagnosis, a slow cognitive decline you've been quietly hoping someone else would name first. Suddenly you need someone there every day, and the system you've been cobbling together isn't enough anymore.

Most families turn to an agency first. It feels like the safe, obvious choice since someone else handles the vetting, the scheduling, the paperwork. For some families, it stays the right choice. But many others, after months of high turnover, unfamiliar faces in their parent's home, and a nagging sense that the care isn't quite right, start asking a different question: is there a better way to do this?

For many families, there is. This guide walks you through every step of hiring a private in-home caregiver for your elderly parent: understanding the real trade-offs compared to an agency, finding qualified candidates, knowing what to pay, handling the insurance and legal pieces, and setting up household payroll so you're protected and your caregiver is paid fairly.

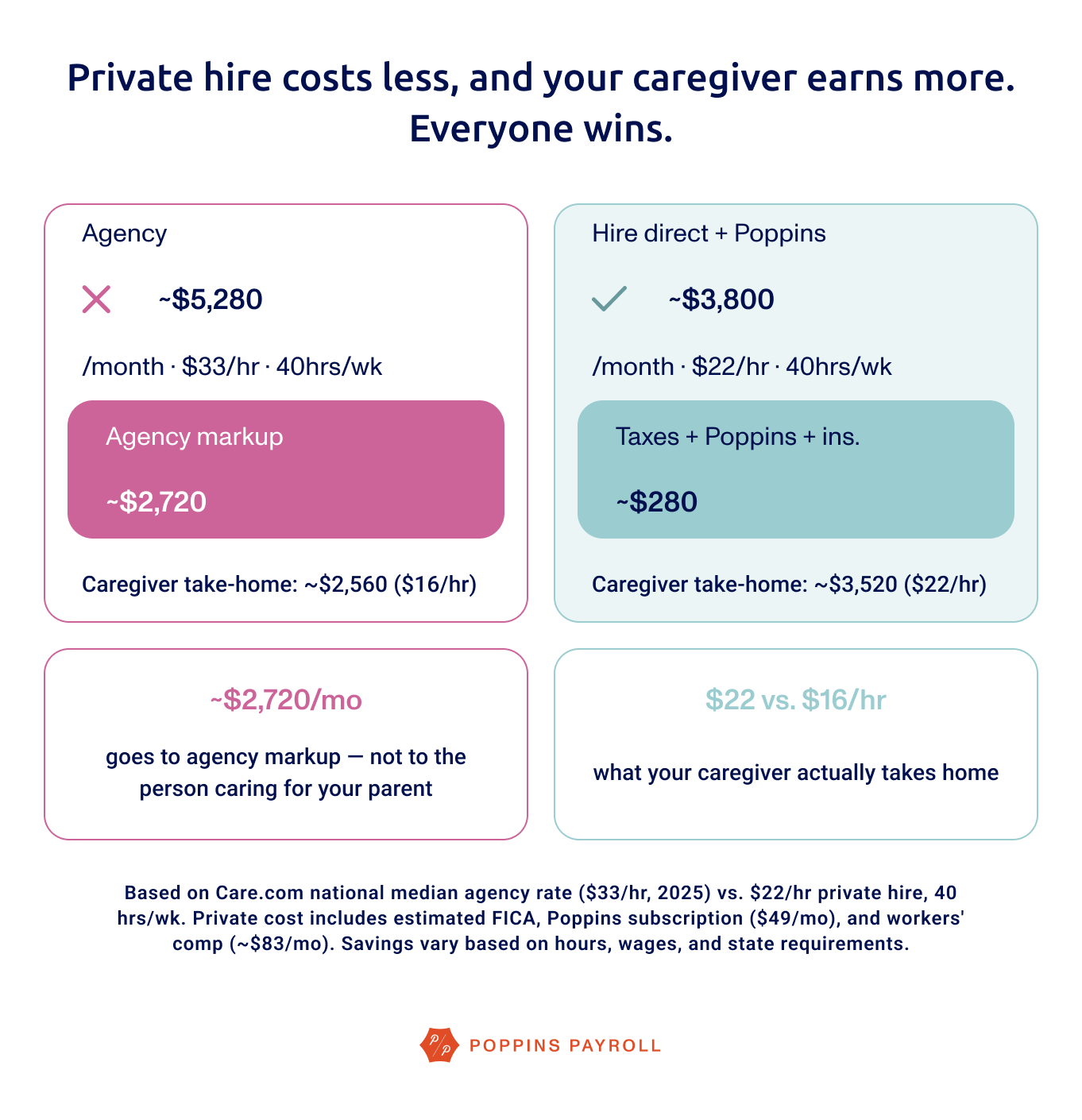

Agency vs. private in-home caregiver for your elderly parent

Private hiring isn't universally better than an agency.

Why private hiring makes sense for many families:

- The cost math. A home care agency typically charges $25-33/hr (national median; often higher in coastal states). Of that, the caregiver takes home roughly $13-18/hr — the agency keeps the rest for overhead, scheduling, and profit. When you hire privately, a much larger share of what you pay goes to the person actually providing care.

- Many experienced caregivers choose private clients. Experienced CNAs and personal care aides who have built strong reputations frequently choose private clients because they earn more and aren't subject to agency scheduling pressure. Families who go through an agency may be paying $30/hr and may have less control over which caregiver is assigned.

- You choose who comes into your home. With an agency, you may have little say over which caregiver shows up, and turnover is common. With a private hire, you interview, you select, and you build a real relationship with one person. For parents living with dementia or Alzheimer's, that consistency can make a significant difference.

Where agencies still have an edge:

- Backup coverage. If your private caregiver calls in sick, there is no agency sending a substitute. If you don't yet have a roster of caregivers to rely on, an agency's bench may be worth the premium. This is a real gap, and one you'll need a plan for before you hire.

- Insurance protection and payroll. Agencies carry their own workers' compensation and liability coverage and handle all payroll obligations. When you hire privately, both of those fall on you. (More on this below — it's manageable, but it requires some setup.)

- Vetting and oversight. Reputable agencies run background checks, verify certifications, and maintain licensure. When you hire privately, all of that is your responsibility.

The insurance and liability question

When you hire and direct a private caregiver for your elderly parent, you become a household employer. That means you're legally responsible for workplace injuries — not an agency, not a staffing firm.

What about homeowner's insurance? Some homeowner's policies offer a workers' comp rider that may cover household employees — but coverage limits are typically capped around $100,000, and many carriers will decline or cancel the rider once they discover your employee provides elder care. Poppins has seen this happen regularly: a family gets a cancellation notice and has to scramble for coverage at the last minute, often at a higher rate. If you have an elder care caregiver, a standalone workers' comp policy is the safer choice. See poppinswc.com for more detail on the differences.

Workers' comp requirements vary significantly by state. Some states require coverage from your caregiver's first day. Others set a minimum hours-or-wages threshold. A few states — like Texas — don't technically mandate it, but you're still personally liable if your employee is injured on the job. A single workplace injury — a back injury while helping someone out of a bathtub, for example — can easily run $10,000–$20,000 or more out of pocket. See your state's specific requirements at poppinswc.com/state-resources.

Poppins partners with Bhalu Insurance to help household employers get covered. The application takes about five minutes, and most quotes are generated in real time.

If your caregiver will drive your parent to appointments or errands, confirm that their personal auto insurance covers them while working. Many personal policies exclude work-related driving.

Workers' comp requirements vary by state. Visit poppinswc.com/state-resources to see your state's rules, or consult Poppins' state resources page.

Where to find private in-home caregivers for elderly parents

- Word of mouth first. Ask other families at your parent's senior center, adult daycare, faith community, or memory care support group. Many experienced private caregivers work entirely through referrals and never post on job boards.

- Area Agencies on Aging. The federally funded Eldercare Locator helps you find your local Area Agency on Aging, which often maintains lists of vetted independent in-home caregivers for the elderly. This is a genuinely underused resource.

- Care.com and caregiver registries. These platforms connect families directly with independent caregivers for elderly parents. Filter by certification (CNA, CPR) and experience with your parent's specific condition.

- Hospice and home health alumni. If your parent has worked with a hospice or home health agency, you may already know a caregiver who has since gone independent. (See the non-solicitation note below.)

- Caregiver community networks. Local Facebook groups and platforms like CareLinx can surface candidates who specialize in elder care.

One important caveat: If the caregiver you want to hire currently works for an agency, their employment contract may include a non-solicitation clause — a provision that prohibits them from leaving to work directly for a family they met through the agency. Violating this clause can expose both you and the caregiver to legal risk. If this situation applies, have an employment attorney review the contract before proceeding. Enforceability varies significantly by state.

Interview questions and red flags

Hiring a caregiver for an elderly parent is unlike any other hiring decision. You're bringing someone into your parent's most private spaces, trusting them with physical care, medication support, and emotional presence.

Ask about:

- Specific experience with your parent's condition — dementia, stroke, Parkinson's, general aging. "I've worked with elderly clients" isn't enough. Ask for specifics.

- Certifications: CNA, CPR, first aid, medication assistance (if applicable). Ask to see documentation.

- References: At minimum two former clients or families. When you call them, ask: "Would you hire this person again?" The pause before the answer tells you as much as the words.

- Backup coverage: Ask directly: "If you were sick or had an emergency, what would happen? Do you have a colleague you could recommend?" A good private caregiver has thought about this.

- Communication style: How do they prefer to update family members — daily texts, a care notebook, end-of-week calls? Make sure it's a fit.

Red flags:

- Vague or hard-to-verify prior experience.

- No references, or references who don't return calls.

- Inconsistencies between what they say in the interview and what references describe.

Compensation

Private caregivers for the elderly earn the full wage you pay them. That means your dollars go further, and you can often afford a more experienced caregiver.

Typical 2026 hourly rates for non-medical personal care:

- Non-metro areas: $18–25/hr

- Major metros (NYC, SF, DC, Boston, LA): $25–35/hr

- Rates increase with experience, specialized certifications, and the complexity of care

A few compensation considerations:

- Guaranteed hours. It's common to guarantee your caregiver a minimum number of paid hours per week, even if your parent's schedule runs short. This protects them and builds a stable relationship.

- Overtime. Most non-exempt caregivers working more than 40 hours per week must be paid 1.5x their regular rate under federal law. California overtime rules for personal attendants are particularly complex — California employers should consult the DLSE or an employment attorney for their specific situation. Overtime rules vary by state — see DOL guidance.

- True employer cost. Your total cost is more than the hourly rate. Add approximately 7.65% for employer-side Social Security and Medicare taxes (FICA) and Federal Unemployment Tax (FUTA), plus your workers' comp premium. See poppinswc.com for an estimate of workers' comp costs in your state.

Onboarding an in-home caregiver for elderly parents: a checklist

A few steps have strict timing — particularly the I-9, which must be completed on or before your caregiver's first day. Work through this list before they start.

Your caregiver agreement should include: start date, job duties, hours per week, daily schedule, hourly rate, overtime policy, guaranteed hours (if applicable), PTO and sick day policy, termination notice period, and a description of any transportation responsibilities. A written agreement protects both parties. Download Poppins' sample caregiver contract as a starting point.

I-9 requirements are governed by federal law. State-specific employment documentation rules vary. Consult an employment attorney if you have questions about your state's requirements.

Setting up household payroll

Once you have your EIN, your caregiver's I-9 and W-4, and your payroll configured, you can add workers' comp coverage through Bhalu using the EIN from your Poppins account.

Poppins handles:

- EIN registration — Poppins registers your Federal Employer Identification Number during setup.

- State account setup — Poppins opens your state and local tax accounts, where applicable.

- Payroll runs — You log hours; Poppins calculates withholdings, issues paystubs, and handles direct deposit.

- Quarterly tax filings — Poppins files and pays your applicable federal and state employment taxes automatically, based on the information you provide, where state obligations apply.

- Year-end W-2 — For active accounts, Poppins issues your caregiver's W-2 in January and prepares the Schedule H filing that you attach to your personal tax return.

Poppins is $49/month plus $10/month per additional caregiver. There's no annual commitment; you can cancel anytime.

Top 10 helpful resources when hiring an in-home caregiver for elderly parents

- Eldercare Locator — find your local Area Agency on Aging and elder care resources

- Care.com — search for independent in-home caregivers

- CareLinx — connect with private caregivers specializing in elder care

- IRS Household Employer's Tax Guide (Publication 926) — household employer tax obligations and payroll requirements

- U.S. Department of Labor Wage & Hour Division — federal wage, overtime, and household employment guidance

- DOL Poster Advisor — determine required workplace posters for household employers

- Poppins Workers' Comp State Resources — state-by-state workers' compensation requirements

- Poppins Workers' Compensation Guide — workers' comp coverage information for household employers

- Sample Caregiver Contract — a downloadable template for caregiver agreements

- Poppins Household payroll account — set up household payroll, tax filings, direct deposit, and year-end tax forms.

Ready to make it official?

Private hiring isn't right for every family. But for families who want more say over who provides care, and who are willing to handle a bit more setup in exchange for a more direct, lasting relationship, it's very doable.

Poppins takes the payroll piece off your plate. EIN, taxes, paystubs, W-2s, quarterly filings — handled. So you can focus on what actually matters.

Start your free trial at poppinspayroll.com

This content is for informational purposes only and does not constitute legal or tax advice. Consult a qualified professional for guidance specific to your situation.

.png)

.png)